This is the story of the worst press release of all time.

A jargon-filled press release so awful that it took down the 16th-biggest bank in the U.S.—and nearly a chunk of the tech industry with it.

Myriad factors contributed to Silicon Valley Bank’s epic collapse, but their comms failure is a major part of the story that a lot of people seem to be missing.

From all accounts, what doomed Silicon Valley Bank wasn’t just that it lost some money on securities. It was that it revealed these losses via a press release so poorly timed and triple-stuffed with confusing jargon that it led everyone to believe a viral rumor that the bank was doomed.

We already know that jargon sabotages your sales and marketing. This is a story about how jargon can take down a $200 billion company.

(Credit to Connie Loizos at TechCrunch and Activation Blizzard’s Lulu Cheng Meservey for their analysis of how SVB’s comms went wrong.)

The backstory

Silicon Valley Bank (SVB) is a storied institution—the go-to-bank for the startup community. During the tech boom over the past decade, startups deposited a lot of cash into SVB, and the bank needed somewhere to put them as a safe haven. So it chose long-term U.S. treasuries and mortgage-backed securities.

This was not the best idea. These investments lost value as interest rates rose, and SVB had to sell them at a $1.8B loss. They knew this disclosure wouldn’t be taken super well, as there were already concerns that SVB was weakened due to dwindling deposits.

So to show that they had things covered, they decided to raise $2B in fresh capital to shore things up.

Silicon Valley Bank had an opportunity to tell a clear story to customers, the media, and Wall Street about how they were getting out of a bad position with the securities and shoring up their bottom line.

But instead . . . they did the exact opposite.

The jargon-filled press release from hell

The trouble all started on Wednesday, when Silvergate—the largest crypto bank—announced it was liquidating.

This made Wednesday not a good day to divulge these losses because—you know—announcing big financial losses right after another tech industry bank goes under is pretty bad timing. Especially after the whole FTX saga put people on edge.

But rather than taking a breath, carefully crafting their story, and working with industry influencers to shape the narrative, SVB’s team yelled YOLO and dropped this jargon-filled monstrosity of a press release at 4:06 ET on Wednesday afternoon.

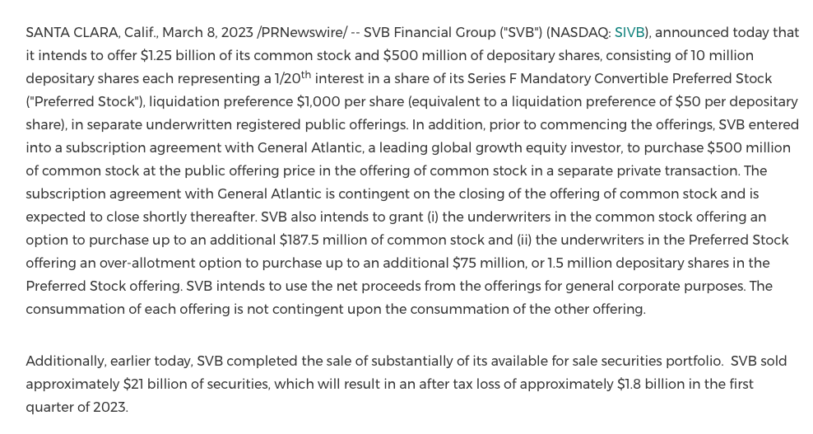

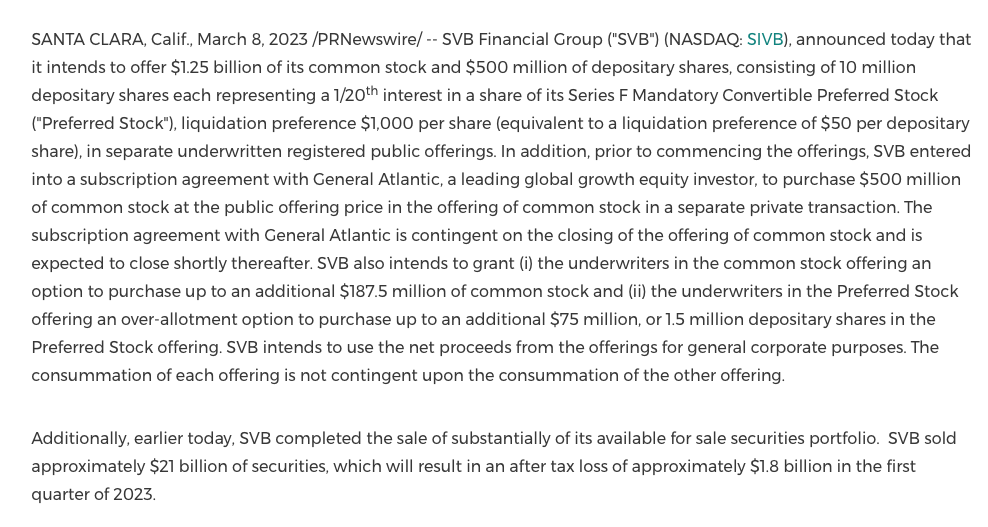

I understand if you have no interest in reading that, so I’ll summarize: it’s basically 250 words of mind-numbing financial jargon—written for underwriters and no one else on the planet—followed by “oh by the way, we lost 2 billion dollars.”

(As the cherry on top, the key sentence meant to explain the sale of securities did not seem to make its way through Grammarly: “Additionally, earlier today, SVB completed the sale of substantially of its available for sale securities portfolio.“)

After the release came out, people started connecting SVB’s disclosure to Silvergate and assumed the worst. As investors Chamath Palihapitiya, Jason Calacanis, David Sacks, and David Friedberg explained on the All-In podcast, panic spread through tech group chats on Thursday after Peter Thiel’s Founders Fund advised its portfolio companies to pull their money from SVB. (Silicon Valley is basically a middle school cafeteria.)

No one wanted to be left holding the bag, so more investors started to whisper to their portcos to pull their funds. The last straw was when SVB CEO Greg Becker hopped on a conference call and told everyone to “stay calm.”

But by the time Becker spoke out, it was already 2:30 ET. The run was already underway, and telling everyone to calm down only induced more panic. (Editor’s Picks: 3 Healthtech VCs on Managing Burn and Raising in a Downturn and How to Survive the VC Deep Freeze.)

A few hours later, investors had pulled $42B from SVB, leaving it with a $958 million cash deficit—meaning that the FDIC needed to take over. This led to a harrowing weekend in which thousands of founders thought their uninsured funds were gone, and tens of thousands of tech employees worried they were about to lose their job.

Ultimately, the government stepped in to guarantee deposits at SVB, but the damage remains. Regional banks are on shaky ground with fears of additional runs, and Silicon Valley Bank—an institution that had powered much of the innovation economy over the past 40 years—is gone.

SVB’s storytelling failure

Humans are storytelling animals. We live in a world of stories. Stories are how we understand the world and make the most important decisions in our lives.

Corporate comms isn’t about positioning and buzzwords, it’s about stories. When you don’t control your own story, you risk everything.

Silicon Valley Bank had an opportunity to tell a story that said, “We lost some money on securities, but we are objectively financially sound and taking steps to further fortify our position.”

Doing so would have meant both not only writing an easy-to-understand press release with a clear narrative, but also working with key industry reporters and influencers to translate the news in a reassuring way. After 40 years supporting the tech industry, SVB had a lot of allies, and they needed those allies to help them tell their story.

Instead, as Meservey noted, they completely ignored two key audience groups: the media and their customers. They crafted a press release with so much financial jargon that only an underwriter could understand it. There was no story about why the bank was making the move. It was like someone fed ChatGPT a financial disclosure report and blindly pressed publish.

And perhaps most shockingly, once the narrative started getting out of control Wednesday evening, they made no effort to change it. They waited 22 hours and 36 minutes to speak out.

By that point, the final death scene had already been written.

This article originally appeared on Mission by A.Team and is reprinted with permission.

Recognize your brand’s excellence by applying to this year’s Brands That Matter Awards before the early-rate deadline, May 3.

{kind=link}