As climate change makes it more likely that many houses in the U.S. will flood—because of rising sea levels, extreme rainfall, or both—federal flood maps, which are used to determine rates for flood insurance, are out of date. A new report maps out where homes now are most at risk, looking at the chances of properties flooding now and 30 years in the future. By the middle of the century, the damage could cost $32 billion a year.

“Climate is not considered in any way in the current mapping structure for FEMA and how they create insurance,” says Matthew Eby, executive director of First Street Foundation, the nonprofit that created the report. “The program started in 1968, and really kicked off in 1970. Some of the maps that exist are still from the ’70s and ’80s.” The maps also show “special flood hazard” areas, but not the individual risk of a particular home, and because of how the federal program was created, also don’t map some regions of the country—only places that opted in.

[Image: courtesy First Street Foundation]Last year, the nonprofit releasedFlood Factor, a tool that homeowners can use to plug in an address and get specific details about the risk of flooding over the lifetime of a typical 30-year mortgage. Using technology like Lidar mapping to understand the topography of a particular house, and advanced models that consider how climate change is increasing heavy rainfall and hurricanes, the nonprofit mapped homes across the country.

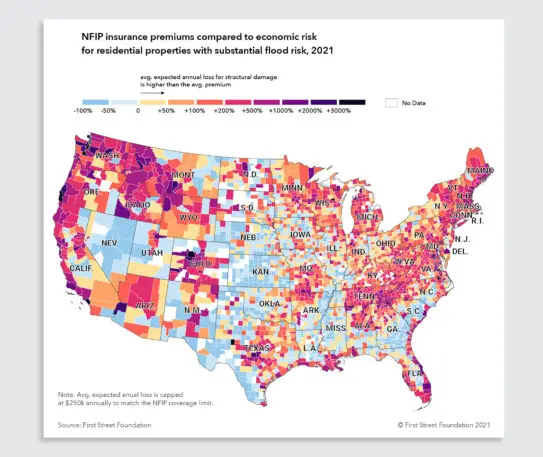

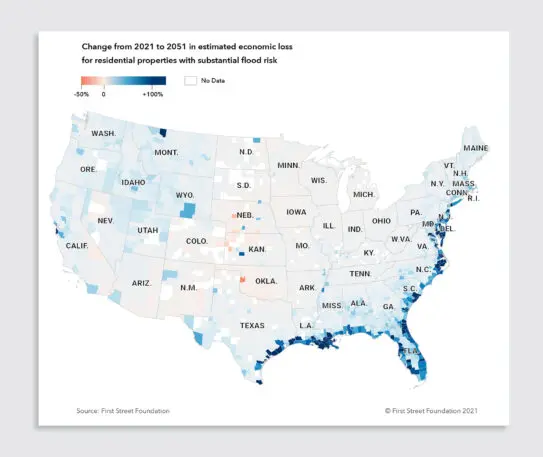

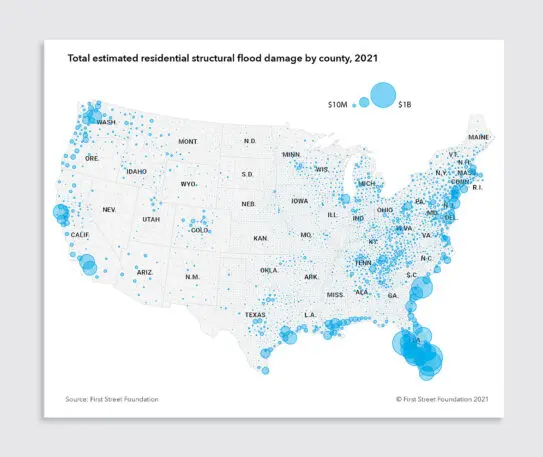

[Image: courtesy First Street Foundation]The new report calculates the cost of potential flooding. Around 4.3 million single-family homes and small multifamily homes have a substantial risk of flooding this year, according to the analysis. While states like Florida and South Carolina are particularly hard hit because of their coastal location, flooding is a risk nationwide. The current FEMA models also don’t consider the direct risk from heavy rain. In cities like Houston, for example, where roads and other pavement blocks water from being absorbed into the ground, “it all pools and collects and funnels into properties that have substantial risk just from rainfall,” Eby says. But most of the homes at greatest risk now aren’t required to buy flood insurance. If they did, the National Flood Insurance Program would have to more than quadruple its rates. This year, the costs from flood damage to homes could total $20 billion. By 2051, that could increase to $32 billion.

[Image: courtesy First Street Foundation]FEMA is currently updating its maps to also begin to look at individual properties and risks like flooding from heavy rain, and will be raising insurance premiums based on new calculations of risk. There will still be challenges for would-be homebuyers who want that information—if a house is at risk but is outside of one of FEMA’s special flood hazard zones, for example, the homeowner won’t be notified. First Street Foundation’s tool can help fill the gap. With the data in hand, homebuyers might choose not to buy a particular house. (Realtor.com and Redfin are both now using First Street’s data on house listings.) Homeowners might invest in raising expensive HVAC equipment off the ground or raising the house itself.[Image: courtesy First Street Foundation]

Policymakers can also use the maps to consider ways to reduce risk neighborhood-wide, like adding parks that can help absorb water. “All of this data is available now to see where these pockets of risk exist and what the building code standards are for those areas, and really think through the development question of not only knowing what is our risk today, but where that risk is evolving,” he says. “How should we as a community, or county, or a state, really think about risks or change building code standards?” In some places, it might mean deciding that a neighborhood is too risky to allow new home construction—or that current residents should get help moving, as is happening in a community in Louisiana that flooded 17 times over the past three decades.

Recognize your brand’s excellence by applying to this year’s Brands That Matter Awards before the early-rate deadline, May 3.

A refreshed look at leadership from the desk of CEO and chief content officer Stephanie Mehta