Jennifer Marie* should be an ideal candidate for life insurance: She’s 36, gainfully employed, and has no current medical issues.

But on September 15 last year, Jennifer Marie’s application for life insurance was denied.

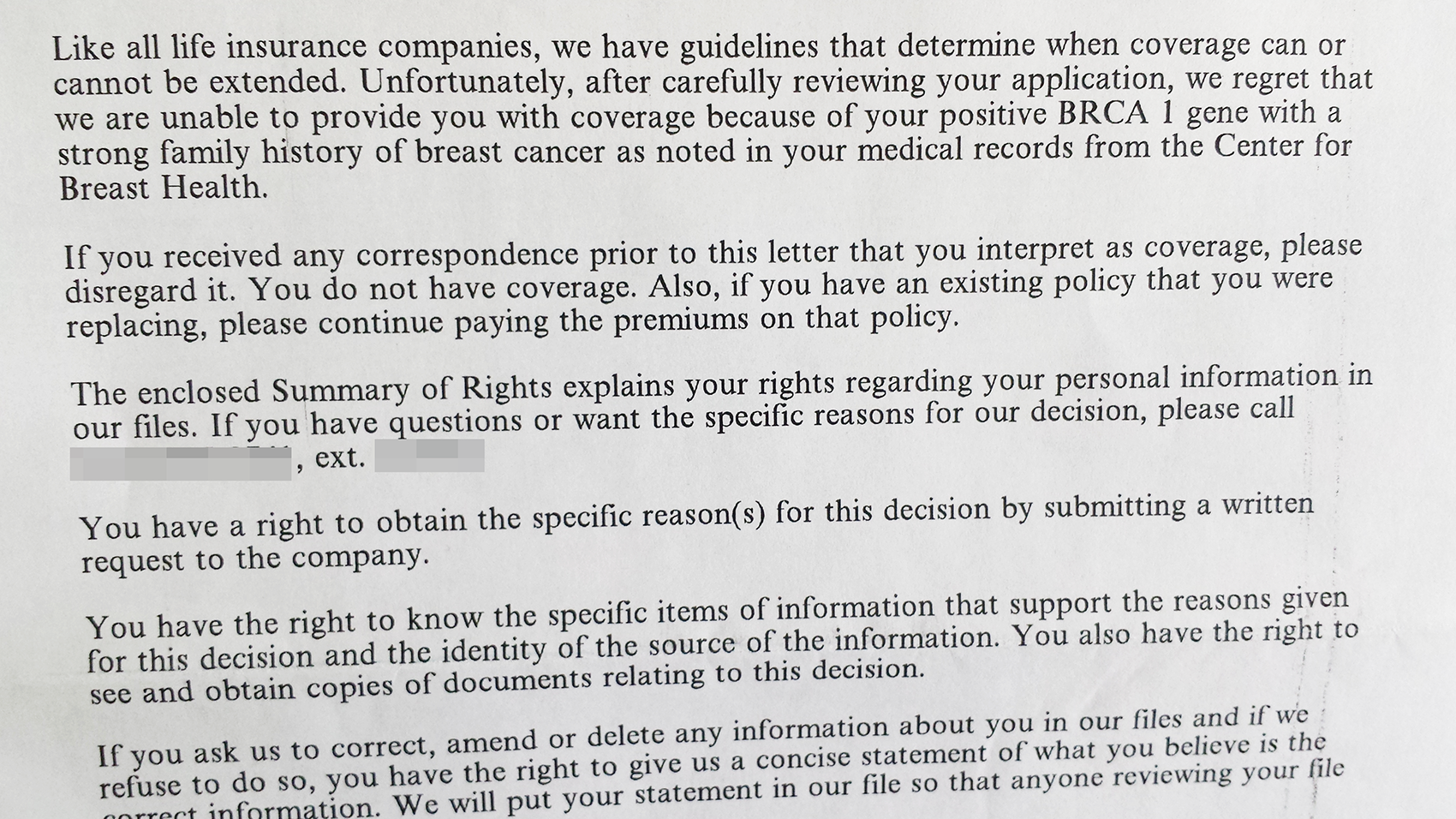

“Unfortunately after carefully reviewing your application, we regret that we are unable to provide you with coverage because of your positive BRCA 1 gene,” the letter reads. In the U.S., about one in 400 women have a BRCA 1 or 2 gene, which is associated with increased risk of breast and ovarian cancer.

Jennifer Marie provided a copy of the document to Fast Company on the condition that she and her insurance company remain anonymous, as she is still hoping to appeal the rejection.

According to recent estimates, 55% to 65% of women who inherit a harmful BRCA 1 mutation will develop breast cancer by the age of 70. By contrast, 12% of the general population will be diagnosed with breast cancer. But the presence of the gene mutation is by no means a death sentence. Not everyone with the BRCA mutation develops cancer, and some informed patients seek highly effective preventative treatments to reduce the likelihood that they’ll ever get sick.

“Those who find out they have the mutation can drastically reduce their risk,” says Laura Esserman, a surgeon and breast cancer oncology specialist at UC San Francisco. “Knowledge is power.”

Since 2008, with the passing of the Genetic Information Nondiscrimination Act (GINA), the federal government has barred health insurance companies from denying coverage to those with a gene mutation. But the law does not apply to life insurance companies, long-term care, or disability insurance. These companies can ask about health, family history of disease, or genetic information, and reject those that are deemed too risky.

Patient advocates say they are increasingly concerned about GINA’s limitations, given the explosive growth of genetic testing. Spending on genetic tests has reached $5 billion annually and is on track to reach $15 billion to $25 billion within a decade, according to a recent study commissioned by the research arm of UnitedHealthcare. The American Medical Association found that physicians use about 2,000 of these tests for 1,000 different diseases. The test makers range from Silicon Valley startups, such as Counsyl and Color Genomics, to biotech giants like Myriad Genetics.

“GINA was designed to free people from fears of discrimination so clinical research can scale,” says Dr. Robert Green, a medical geneticist at Brigham and Women’s Hospital in Boston. “I am now wondering whether it worked or not. People started off afraid and they clearly still are.”

The Rise Of Genetic Tests

When GINA first passed in 2008, genetic tests were expensive and not all that common. In 2011, the late Apple CEO Steve Jobs spent $100,000 to discover the genetic basis of the cancer that killed him. Today, a company called Illumina can sequence a person’s whole genome for $1,000.

Recent advancements in the field of genetics have opened up major opportunities for medical progress, including the promise of earlier detection of disease and more personalized treatments that could wring savings from the country’s multi-trillion dollar health care tab. The White House’s $215 million Precision Medicine initiative is reliant on the further dissemination of genetic tests to screen people for diseases, and identify those who are unable to safely take medicines.

The BRCA test is now available for as little as $250, enabling many patients to pay for it out of pocket. Dozens of lab-testing companies have developed a BRCA test, including Color Genomics and Counsyl. The test even has a celebrity spokesperson in the form of Angelina Jolie, who underwent a preventive double mastectomy in 2013 after learning about her cancer risk, and penned a widely circulated op-ed on her experience.

As these tests become more pervasive, patient advocates are ramping up their campaign to end so-called genetic discrimination.

“Our biggest concern is that people aren’t aware that this information can be used against them,” says Lisa Schlager, vice president of community affairs at FORCE, a nonprofit group that supports women with hereditary breast and ovarian cancer.

Northwestern Mutual, a life insurer that has been fairly explicit about its approach, does not require an applicant to undergo a genetic test. But company spokesperson Betsy Hoylman says that actuaries do routinely ask about medical and diagnostic testing, which may include genetic testing, in order to “treat existing and prospective customers fairly.”

“A consumer’s failure to cooperate during the underwriting process may result in an insurance company declining to issue a policy,” says Hoylman. Oncologists say this form of discrimination might discourage people from getting genetic tests.

Schlager has seen both men and women sharing their experiences about genetic discrimination on FORCE’s private Facebook group and other online forums. While her group hasn’t done any research or polling on the topic, they believe it is widespread enough to warrant more attention. “It’s a weird loophole,” she explains. “But there are a lot of those. And these Precision Medicine initiatives haven’t really caught up.”

But some health insiders say that it won’t be easy to change the laws. Sharon Terry, a patient advocate who spent more than 14 years fighting for GINA, says the opposition from the insurance industry remains as strong as ever. Terry is the CEO of a Washington D.C.-based nonprofit called Genetic Alliance that advocates for the health benefits in the field of genetic research.

“At the beginning of this decade-long saga, the bill [GINA] included every type of insurance,” says Terry. But early proponents of the bill threatened to drop their support if it included disability, life insurance, and long-term care. Genetic Alliance ultimately acquiesced to their demands.

“It was the right thing to do,” says Terry. “The bill would never, ever, ever have passed in any form. Many bills don’t, and the opposition on this one was strong.”

On a state level, Terry has seen more progress in recent years. California passed a bill called CalGINA that not only prohibits genetic discrimination in employment and health insurance, but also in housing, education, mortgage lending, and elections. Oregon and Vermont also have broad regulations prohibiting the use of genetic information in life, long-term care, and disability insurance.

Not All Insurance Is Created Equal

The industry makes the case that the business model would crumble if companies are forced to accept those with a high risk of cancer and various genetic diseases into the pool.

There is some truth to this argument. Brigham and Women’s Hospital’s Dr. Green studied the behavior of those who learned via a genetic test that they were predisposed to Alzheimer’s Disease. These patients were five times as likely to buy long-term care insurance than those in a control group.

And rather uniquely, health insurers are able to offset their risk by taking in monthly premiums from young and healthy Americans (the Affordable Care Act’s “Individual Mandate” requires that many people get health insurance or face a penalty). By contrast, a decision to purchase life insurance or long-term care insurance is optional. Those who apply for policies might have reason to believe that they need additional protections.

“All forms of insurance are not created equal,” says Mark Rothstein, a founding director of the Institute for Bioethics, Health Policy and Law at the University of Louisville School of Medicine. “I see health insurance on one side of the spectrum, life insurance on the other, and disability and long-term care somewhere in the middle.” Long-term care, for instance, is covered in part by Medicaid.

“The big question for our society is where we want to locate the risk.” Rothstein has spent over a decade on this issue, and wrote a book on the topic in the late 1990s: Genetic Secrets: Protecting Privacy and Confidentiality in the Genetic Era.

As Rothstein explains, all life insurance companies engage in a certain degree of “discriminating between claims.” But there are limits. Most life insurance companies don’t discriminate on the basis of race, despite the health disparities between different ethnic groups. Many companies, however, do distinguish between claims on the basis of gender, as women tend to live longer than men.

It remains to be seen whether society will continue to view it as acceptable for life insurers to discriminate on the basis of people’s genetic information, particularly if it’s a genetic marker like BRCA 1/2 that doesn’t always result in cancer. A slew of recent studies have shown that those who test positive for the gene mutation and subsequently initiate preventative measures, like MRI screenings and mammograms, are very likely to catch cancers earlier. And some opt for surgical procedures, like mastectomies, which drastically decreases their risk. Angelina Jolie claimed that after taking preventative measures, her risk of getting breast cancer dropped from 87% to 5%.

But Rothstein fears that many life insurance companies aren’t sophisticated enough in their knowledge of genetics to delineate between the various types of tests, or even fully understand the results. James Heywood, founder of a startup called PatientsLikeMe, says he was denied life insurance from one insurance company after his brother passed away from a progressive neurodegenerative disease called ALS. Heywood had taken a test and shared the results, which showed that he didn’t have the risk factor for the disease.

“It’s an industry that is hundreds of years old,” says Rothstein. “They make a lot of money doing things the way they’ve always done it.”

“Chilling Effect”

GINA’s loophole hasn’t just caught the attention of patients’ rights groups. Medical researchers are also growing increasingly concerned that it will set back their clinical trials and studies.

Green directs a randomized trial to study gene sequencing in adults called the MedSeq project, which relies on patients agreeing to store their genome sequencing data in their medical record. As he recently reported in the New England Journal of Medicine, 25% of patients who declined to participate in the study cited fear of discrimination from life insurance companies as their primary reason.

Green expects that more patients will bow out of clinical studies and genetic tests as they become aware of the downsides.

“Before GINA passed, a lot of people were afraid that this new era of genetic testing wouldn’t include proper protections for patients,” says Green. “But there’s still reason to be afraid that companies will discriminate against whole families.”

Dave*, a father from Washington, D.C., who agreed to speak on the condition of anonymity, recently learned that his sister has the BRCA gene. His doctor suggested that he get a genetic test, as men with harmful BRCA mutations have an increased risk of prostate cancer. Dave, who says he’s heard copious “horror stories” of people being denied life insurance, ultimately decided against the test.

“On the one hand, I know that there is something I could do that could help prolong my life,” he says. “But I’m terrified that my insurance company will find out if I get a positive result.” If a life insurance company uncovered that a patient withheld valuable information, they might make a case for “guilt by omission.”

“This is not the calculation I want to be doing when it comes to my health.”

Finding A Middle Ground

With the increasing prevalence of genetic tests and tools, the debate on discrimination in the context of life insurance has become more urgent and complex. In recent months, Terry’s group Genetic Alliance has been fighting against proposed rules that would allow employers that offer wellness programs to penalize employees and their spouses if they refuse to participate in various questionnaires and surveys about their health. Genetic Alliance argues that such bills would directly undermine GINA.

Patient advocates have pushed for an extension of GINA for many years without success. But some experts see a middle-ground approach. Rothstein suggests that insurers should at a minimum “offer a life insurance policy covering a minimal amount at an affordable rate and with no health questions (including about genomics) asked.”

In the meantime, some genetic-testing companies are taking steps to educate patients about their risks so they won’t be blindsided like Jennifer Marie. Color Genomics says information about genetic discrimination is available on its website, and its genetic counselors will educate patients about the issue. 23andMe, which previously offered BRCA 1/2 tests, says it is in support of state and federal laws to “add life, disability, and long-term care to a list of protections.”

Rothstein says that there’s no simple or easy short-term solutions to the problem of genetic discrimination.

“I wish that we could snap our fingers and end the problem,” Rothstein says. “But it’s a very complicated one that many of us have been working on for years.”

Related: Should This Fast Company Editor Take 23AndMe’s Spit Test?

*The last names of sources Jennifer Marie and Dave have been left out to protect their privacy.

Have you been denied insurance because of a genetic test result? Get in touch: Cfarr@fastcompany.com

Recognize your brand’s excellence by applying to this year’s Brands That Matter Awards before the early-rate deadline, May 3.